In today's financial landscape, conventional profit metrics no longer fully reflect the realities companies face in a climate-constrained world. Greenhouse gas emissions have direct, quantifiable economic consequences, yet they are frequently omitted from traditional financial reporting. EcoMap addresses this gap by integrating the environmental costs of carbon emissions into financial analysis. By calculating climate-adjusted profit, EcoMap provides a more accurate picture of a company’s overall performance, offering stakeholders clearer insights into the monetary implications of carbon emissions and environmental impacts

Understanding Profit Adjusted for Financial Climate Risk

Profit adjusted for financial climate risk provides a more complete picture of corporate financial performance by integrating environmental costs directly into financial metrics. These environmental costs primarily stem from greenhouse gas emissions, categorized into Scope 1, Scope 2, and Scope 3 emissions. Scope 1 emissions are direct emissions from a company’s owned sources, Scope 2 covers indirect emissions from purchased energy, and Scope 3 encompasses all other indirect emissions occurring within a company’s value chain. Monetizing these emissions translates them into explicit financial costs, offering a clearer lens through which to assess overall performance, revealing profitability after fully accounting for their carbon footprint.

Why Does Climate Adjustment Matter?

Incorporating climate adjustments into financial performance assessments matters because carbon emissions represent significant hidden financial risks. Globally, operational environmental costs linked to Scope 1 and 2 emissions accounted for roughly 34% of corporate operating profits in 2023, and when considering Scope 3 emissions from value chains, this figure exceeded operating profits significantly. This clearly indicates that businesses often overlook the true financial magnitude of their carbon cost exposure. Failing to account for these environmental costs leaves companies and their investors vulnerable, as financial performance becomes misaligned with the underlying reality of climate risk.

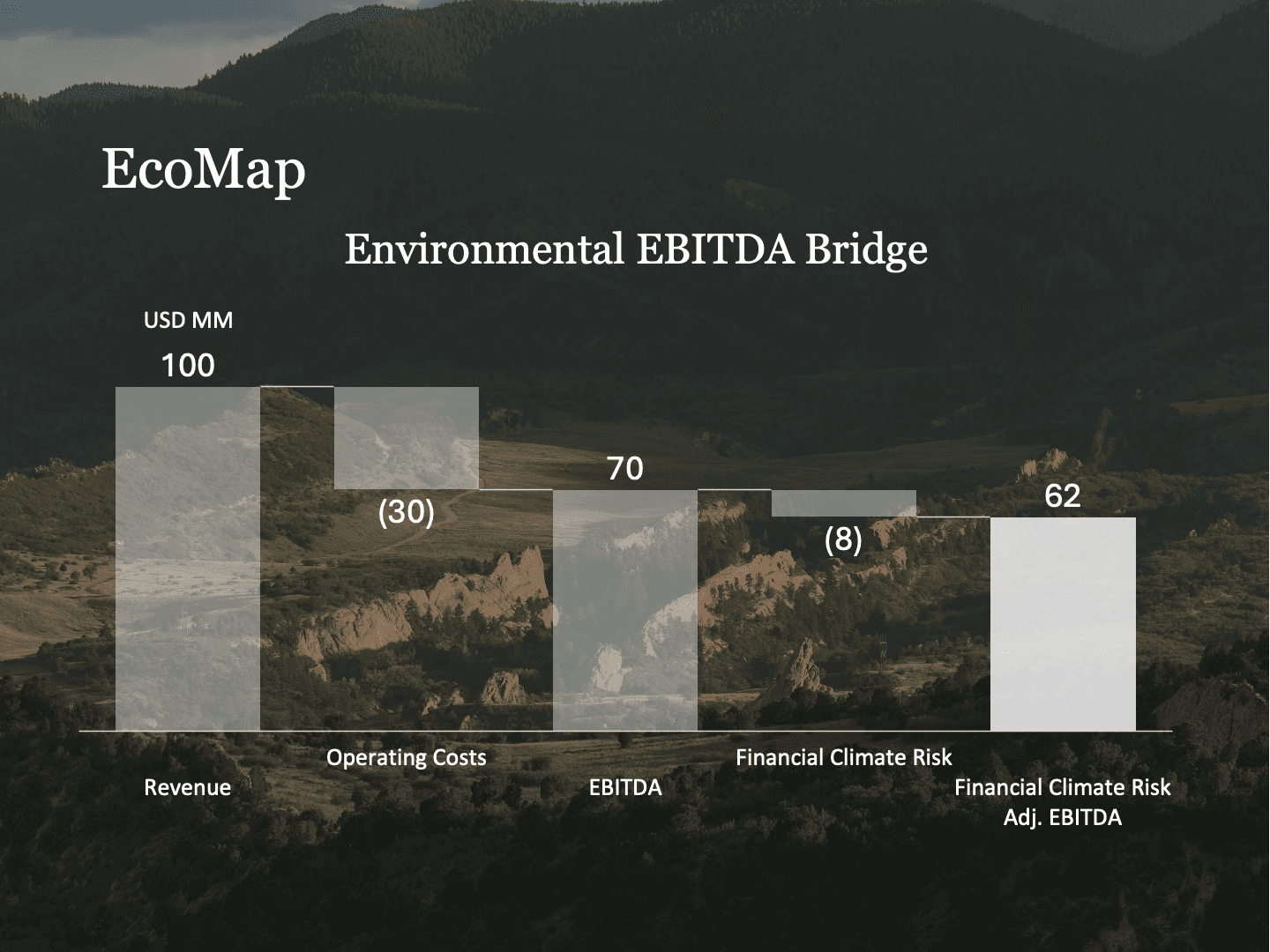

Integrating Climate Costs into Financial Metrics

Integrating environmental costs into traditional financial metrics, such as EBITDA and EBIT margins, provides critical insights into how effectively companies manage these costs relative to their revenues. For instance, a company might report a strong conventional EBITDA margin, but show a significantly lower Environmental-Adjusted EBITDA margin once the financial impact of carbon emissions is accounted for. An EBITDA bridge can illustrate this transition effectively, showing how operational environmental costs materially influence traditional profitability measures. By clearly observing the tangible financial impact of emissions, stakeholders can better assess environmental efficiency and identify financial vulnerabilities linked to operational carbon risks, facilitating informed strategic decisions.

Regulatory and Market Drivers

The transition toward climate-adjusted financial analysis aligns with emerging global regulatory frameworks and standards such as the EU's Corporate Sustainability Reporting Directive (CSRD) and ISSB-aligned climate data standards. Emphasizing double materiality, these frameworks encourage businesses to disclose not only the financial impacts climate change may have on their operations but also how their activities contribute to broader societal costs. Transparent climate disclosures enable investors, policymakers, and other stakeholders to make informed decisions, ensuring that environmental considerations are central to financial and operational planning.

Use Cases for Companies and Investors

Integrating climate adjustments into financial analysis empowers businesses and investors to proactively manage supply chain risks, operational efficiencies, and strategic planning. Through peer-level climate risk comparisons, decarbonization benchmarking, and clear assessments of transition risks embedded in operations, companies can prioritize actions to reduce environmental costs. Such strategic alignment facilitates the decoupling of emissions from revenue growth, a critical goal for businesses committed to sustainable profitability.

Recognizing profitability adjusted for financial climate risk is crucial for maintaining competitive advantage and securing investor confidence in a rapidly evolving market landscape. Investors increasingly prioritize transparent climate-adjusted financial metrics to identify sustainable investment opportunities and manage long-term risks effectively. Companies integrating environmental costs into core reporting enhance their strategic resilience, optimize operational efficiencies, and signal commitment to sustainability, aligning financial performance with broader stakeholder expectations.